The global spotlight in Malaysia as it emerges as a semiconductor powerhouse.

The China Plus One (C+1) strategy has gained traction since it was first proposed in 2013. This strategy involves multinational companies (MNCs) and investors complementing their China operations with investment in another country, often referred to as the “+1,” to lower costs, diversify risks, and access new markets. Given tectonic shifts in the global economic landscape and economic security, this approach will accelerate further.

Among Malaysia’s advantages for the C+1 strategy are its strategic geographical position as a shipping and logistics hub, diversified economic sectors, products, and markets, combined with political stability and good governance. The country also boasts a skilled workforce, well-developed infrastructure, and a business-friendly environment. Additionally, Malaysia’s geographical proximity to China and its membership in the Association of Southeast Asian Nations (ASEAN) make it an attractive investment destination.

Malaysia has been attracting investments as part of the C+1 strategy, particularly in the semiconductor and chip manufacturing sector. The China+1 strategy has contributed to increased chip investments in Malaysia as companies seek to diversify their supply chains and reduce dependence on China. As tensions between the United States and China have risen, there has been a push to secure chip supply chains outside of China. Malaysia is well-positioned to capitalise on this strategic shift and attract foreign investment.

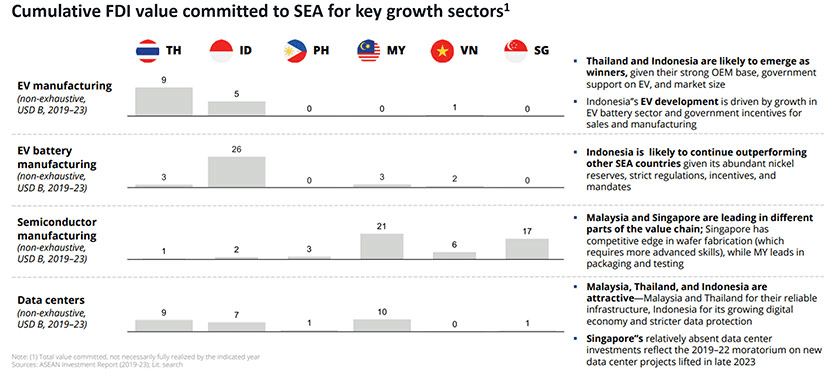

Figure 1: Malaysia is among the Southeast Asian countries that are well-positioned in high-growth, next-generation sectors

Source: NAVIGATING HIGH WINDS, South-East Asia Outlook, 2024-2034 by Angsana Council, Bain & Company, DBS

Malaysia is the leader in SEA by FDI (foreign direct investment) in the semiconductor sector. According to the Malaysian Investment Development Authority (MIDA), major brands like Intel, AMD and Bosch established early operations, joined later by Infineon, Micron and many others. Malaysia has successfully developed homegrown champions such as Inari, Vitrox, Oppstar, SkyeChip and Pentamaster as part of the global value chain. Over the years, this fostered a robust local supply chain and skilled talent pool.

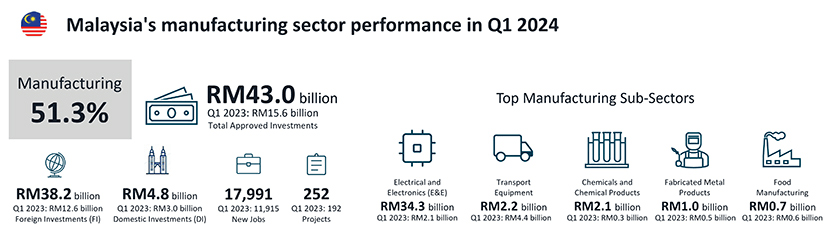

Figure 2: Malaysia’s manufacturing sector performance in Q1 2024

Source: Malaysian Investment Development Authority (MIDA)

The country’s manufacturing sector has attracted significant FDI in recent years, particularly in the E&E segment, with RM34.3 billion (US$7.9 billion) in approved investments in Q1 2024. Leading companies recently announced their investment include Intel, which set up a US$7 billion plant; Micron, which plans to invest another US$1 billion to set up its second assembly and testing facility; and Infineon, which has allocated an additional €5 billion for Phase 2, on top of the original €2 billion for Phase 1, to construct the silicon carbide power fabrication plant.

The Malaysian government recently unveiled the National Semiconductor Strategy (NSS), indirectly declaring the country’s intention to cement its position as a leading international hub for semiconductor manufacturing and innovation while aiming to build a strong base in chip design. Backed by an initial RM25 billion (US$5.33 billion) allocation, the plan provides a clear roadmap for the country’s move up the global technology value chain. The NSS plays a significant role in Malaysia’s ambition to strengthen its position in the global semiconductor industry and participate in the C+1 strategy.

Amidst the growing adoption of the C+1 strategy, the outlook remains positive. The industrial and logistics sector continues to attract foreign investors, which is expected to contribute to the growth of capital values in the market as investor interest remains strong.

马来西亚仍是中国+1战略的领跑者(JLL)

随着马来西亚成为半导体强国,全球的目光聚焦于此。

自2013年首次提出以来,中国+1(C+1)战略逐渐获得广泛关注。这一战略涉及跨国公司(MNCs)和投资者,在继续运营中国业务的同时,选择在其他国家进行投资,这个国家通常被称为“+1”,目的是降低成本、分散风险并开辟新市场。鉴于全球经济格局和经济安全的剧烈变化,这一策略的推动将进一步加速。

马来西亚在C+1战略中的优势包括其作为航运和物流枢纽的战略地理位置、多元化的经济行业、产品和市场,结合政治稳定和良好的治理。此外,马来西亚还拥有一支技术熟练的劳动力、完善的基础设施和有利的商业环境。更重要的是,马来西亚靠近中国,并且是东南亚国家联盟(ASEAN)的成员,使其成为一个有吸引力的投资目的地。

马来西亚一直在吸引作为C+1战略一部分的投资,尤其是在半导体和芯片制造领域。中国+1战略促使马来西亚吸引了更多的芯片投资,因为企业希望多样化供应链,减少对中国的依赖。随着美中之间的紧张局势加剧,各方开始推动确保芯片供应链脱离中国,马来西亚在这一战略转变中具备了良好的优势,能够吸引外国投资。

图1:马来西亚在东南亚国家中,处于高增长、下一代行业的有利位置

来源:ANGSANA COUNCIL,《东南亚前景展望 2024-2034》,Bain & Company,DBS

马来西亚在东南亚地区半导体领域的外商直接投资(FDI)方面处于领先地位。根据马来西亚投资发展局(MIDA)的数据,像Intel、AMD和Bosch等大品牌早早在马来西亚设立了运营,随后Infineon、Micron等公司也加入了这一行列。马来西亚成功培养了本土企业如Inari、Vitrox、Oppstar、SkyeChip和Pentamaster,成为全球价值链的一部分。多年来,这促进了本地供应链的稳健发展和人才储备。

图2:马来西亚2024年第一季度制造业表现

来源:马来西亚投资发展局(MIDA)

近年来,马来西亚的制造业吸引了大量外商直接投资,特别是在电子和电气(E&E)行业,2024年第一季度批准的投资额达到343亿马币(79亿美元)。近期宣布投资的领先公司包括Intel,计划建立一个70亿美元的工厂;Micron,计划投资10亿美元建设其第二座组装和测试设施;以及Infineon,其为第二阶段拨出了额外50亿欧元,这在原本20亿欧元的基础上增加,用于建设硅碳化物功率半导体制造厂。

马来西亚政府近日发布了国家半导体战略(NSS),间接宣布该国希望巩固其作为全球半导体制造和创新领先国际中心的地位,同时旨在建设强大的芯片设计基础。该计划得到了最初250亿马币(53.3亿美元)的资金支持,提供了马来西亚进入全球技术价值链的清晰路线图。国家半导体战略在马来西亚加强其在全球半导体产业地位和参与中国+1战略中扮演着重要角色。

在中国+1战略日益广泛采用的背景下,前景依然乐观。工业和物流领域继续吸引外国投资者,这预计将促进市场资本价值的增长,投资者的兴趣仍然强劲。